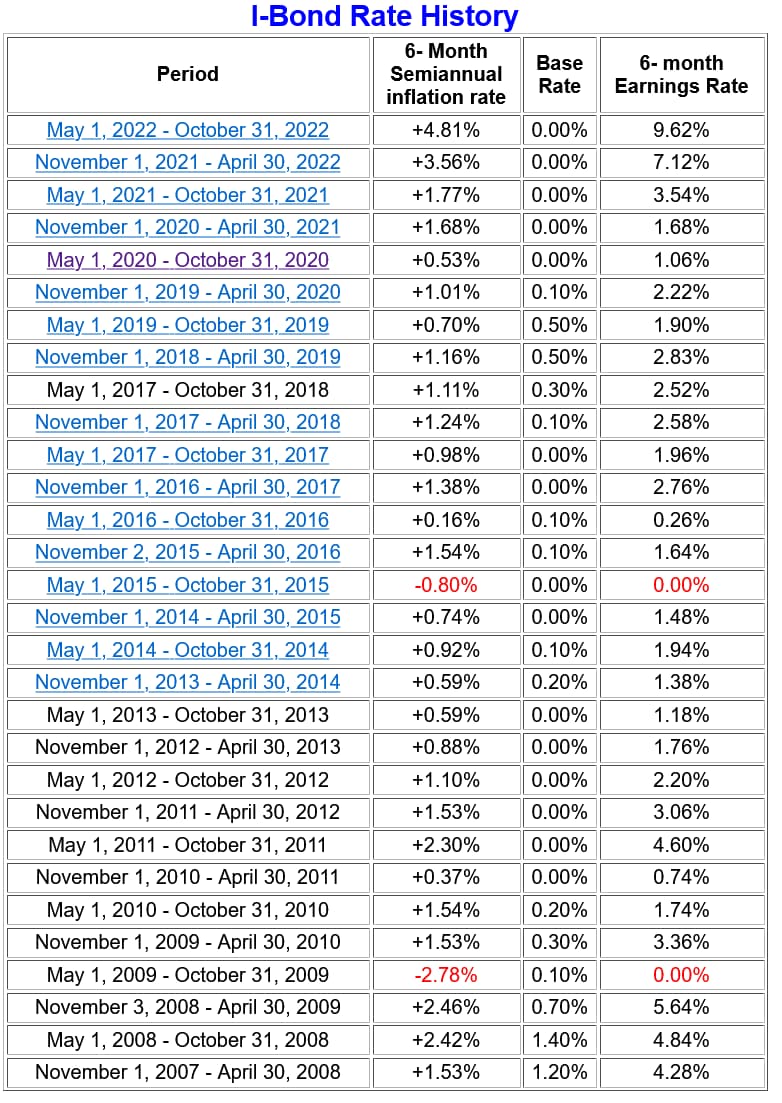

I-Bonds. I repeat…Look at them. Consider them. No, 9.62% won’t last much longer (October), but when you can diversify 20K per household and it is guaranteed by the federal government, it’s a must for many households. 3-month interest penalty (after 12 months holding) is OK.

so if the invigorated interest I-Bonds is partially as a way to decrease the money supply, is it a method the Fed is using to abate inflation? and if this attempt works and the inflation rate comes down, that means it reduces the yield? the fixed rate component of an i-bond doesn’t change and is currently at 0%

would it then be better than the equity market? mid to long term, since these i-bonds are 10 year bonds

IBonds exist just as a saving option that the government decided to create. There isn’t any active effort to curb inflation using them, they are just linked to inflation by law.

They are actually 30 year bonds, but you can cash them out after one year (forfeiting 3 months of interest if you cash out before 5 years).

Long term the expected real return is 0% since they are just pegged to inflation. In the short term since inflation is high and the bonds are risk free, the interest rate is attractive.

IMO, in terms of long term investments they aren’t a great deal, but if you’re willing to lock up your money for at least a year then they are much better than high yield saving accounts. Good for emergency funds and for saving for expenses that are only a couple years away (maybe a house down payment or something similar).

To simplify…an IBond should be compared to the yield you are receiving on your “safe” money, such as CDs, MM funds, checking accounts, etc… They should not be lumped into the same conversation that discusses stocks etc…

Right now, it’s a pretty good bet. Probably next year too. If yields/inflation reverse, get out of the IBond, if you wish, and move the money as you see fit.

Sold Occidental Petroleum at $74 1/2 this morning. This was a Marc Chaikin recommendation that I mentioned months ago at $54. I still like the stock (so does Warren!) since I’m a tad too tech-heavy.

His newsletter is the only one I receive. It’s worth every penny…x a million! I pay $69 per year, although the initial price may be less.

Nobody celebrating inflation numbers today. Slight increase in July instead of a slight decrease. Annual 8.3% with a crappy 6.3% core.

BUT…new IBond rates will be announced in less than two months and they will remain high. If you already bought this year, in January, you’ll earn November’s rate.

Definitely a long-term play. In most cases like this, I would say it is speculative; however, historically, betting against Elon Musk has been a losing proposition.

I think it has a ways downward to go still. I think Elon highly inflated the value during the IPO. No shade though, I invested in SKHY after they ran up and am getting burned on them as well. Although they are at least making boatloads of money, the question is for how long. I think it will go on longer than people anticipate.